Video-on-demand (VOD) streaming services are increasingly identifying growth opportunities in Africa, as other markets across the globe slow down.

SA’s VOD market posted the highest revenue on the continent in 2022, at R4.3 billion, with further growth forecast over the next three years.

This is one of the key findings of PwC’s Africa Entertainment and Media Outlook 2023 – 2027 report released yesterday in Johannesburg.

It covers the entertainment and media (E&M) industries across three regions – Kenya, Nigeria and SA – as the sectors are seen as considerable economic drivers on the continent.

The report highlights that the E&M sectors that were adversely impacted by COVID-19 are emerging from the grips of the pandemic, rebounding relatively well after having to undergo a process of reinvention.

Despite 2022 being a challenging year for Africa’s E&M industry, strong growth is expected across multiple segments going forward, with all markets forecast to be ahead of pre-COVID revenue levels.

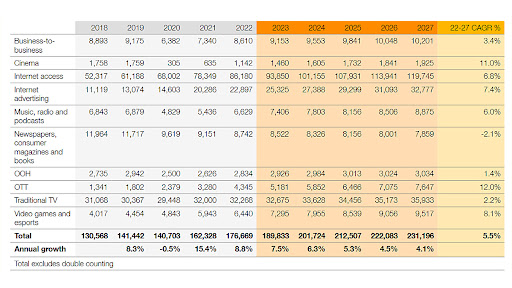

SA’s E&M growth stabilised in 2022 to 8.8%, down from 15.4% in 2021. With most segments up from pre-pandemic levels, total revenue is forecast to increase from R176.7 billion in 2022, to R231.2 billion in 2027, at a 5.5% compound annual growth rate.

Local markets expected to see significant growth include over-the-top (OTT) video, internet advertising, music, radio, podcasting, gaming and e-sports, says the report.

Streaming will be boosted by intensified market competition, as new local users take out subscriptions and existing customers upgrade and add more options to their packages, it says.

Alinah Motaung, PwC Africa E&M leader, tells ITWeb: “There is a slowdown of OTT video globally, as players look to Africa for growth opportunities. Africa has a growing, young, tech-savvy population and they are the ones driving growth and access on these streaming platforms.

“The likes of Netflix, Amazon Prime Video and Disney+ are carving out a market in Africa.”

South African E&M in the coming years will be boosted by the fierce competition between global platforms, and domestic options such as e-VOD and MultiChoice’s Showmax. There are many other new players that have emerged in this space that target Africa, she adds.

Paramount announced its streaming platform, Paramount+, would launch in Africa by 2024, further intensifying competition, notes Motaung.

Factors leading to lower consumption volumes of streaming services globally include increasing competition, falling stock markets, rising interest rates and the tapering off of pandemic-era growth trends, she continues.

African streaming platforms are increasingly tailoring themselves to African viewers, providing local content to better compete with services that have an established global footprint.

For instance, in March, MultiChoice announced it would create a new Showmax group, in which it would own a 70% stake, with the remaining 30% held by Sky and NBCUniversal.

According to PwC, this partnership enables Showmax to lean on content from Sky and NBCUniversal, including live football games from the English Premier League. Showmax intends to relaunch in late 2023 and will utilise technology from NBCUniversal’s Peacock streaming service.

“A challenge for VOD companies looking to succeed in Africa will be ensuring their content is easily consumable through mobile devices, given how much more abundant smartphone ownership is.

“Obstacles that still face streaming across Africa are high price points, unstable internet connectivity and a lack of flexibility in payment options. Service providers will need to be optimised to ensure services consume less data, while also providing adequate viewing quality,” adds Motaung.

Revenue from spending on internet access-related products and services grew to R86 billion in 2022.

SA, like the rest of the continent, remains a mobile-first country and data consumption is up by over 25% to 61.5k Petabytes (PB) from 19.5k PB in 2022.

The PwC research found the growth of internet penetration in SA is increasingly boosting internet advertising. Locally, internet advertising grew to R22.8 billion in 2022 and will increase by over 7% during the next five years.

“While the biggest spend is still from internet access, it is only the fifth-fastest-growing segment. The fastest-growing segment is OTT video, then cinema, followed by video games and then internet advertising,” notes the report.

Revenue for music streaming, radio and podcasts grew to R6.6 billion in 2022, according to the report.

Charles Stuart, PwC South Africa E&M partner, points out the music streaming market continues its march across SA, Nigeria and Kenya, with strong growth being experienced in music streaming subscription revenue.

“Spotify has grown a sizeable foothold in SA. Local users have streamed more than 1.2 billion hours of music since Spotify launched in 2018. The service has benefited local artists; however, South African musicians have struggled to generate a significant income from music streaming.”

Video games and e-sports continue to show good growth, reaching revenue of R6.4 billion in 2022.

This segment is seeing a shift from traditional devices (PC and game consoles) to mobile over the forecast period. Regulations in some countries, such as China, are restricting the segment’s growth.

In SA, casual and social gaming is increasing, with this market forecast to grow by over 8% to reach R9.5 billion in 2027 from R7.2 billion in 2023.

“SA leads the three markets covered in terms of video games and e-sports revenue, with strong growth being recorded in 2022. This was especially prominent within the e-sports category, with total e-sports revenue up almost a third year-on-year,” according to the report.

Share